It’s the existential challenge faced by asset managers all over Wall Street: Surrender to the fee-killing exchange-traded fund boom—or keep bleeding assets and risk extinction. Now they’ve hit on a way to fight back.

Investment giants are lavishing billions of dollars in a bet that they can bring the personal touch back to an investing world dominated by mass-market index funds. They include Morgan Stanley and even dominant ETF and index players BlackRock and Vanguard Group. They’re all racing to offer software that can create a unique index for every investor and then let them buy all the shares in it directly. The result? A mashup of active and passive investing that’s supposed to offer the best features of both.

These products come with dull-sounding labels such as “custom indexing” or “direct indexing” that belie the radical potential of the approach—a kind of Spotify for investing that allows people to mix their own fund. “Custom indexing really is the thing that’s going to drive the future of asset management,” says Patrick O’Shaughnessy, whose then-$6.4 billion firm was scooped up in September by Franklin Resources Inc., the fund manager better known as Franklin Templeton, as part of the trend. “It’s our responsibility to let people make their own choices.”

To critics, it’s an attempt to rebrand active investing just to extract fees higher than most ETFs charge. But to the likes of O’Shaughnessy, it’s helping investors take back control of their investments from the index-following robots that are sinking their cash into companies on autopilot.

Why Are Personalized Stock Portfolios Becoming Popular?

One of the things that made O’Shaughnessy Asset Management (OSAM) attractive to Franklin Templeton is a custom-indexing platform named Canvas. Launched in late 2019, it had already ballooned to $1.8 billion in assets by the time of the acquisition. Canvas is aimed at financial advisers, who can use it to create individualized investment portfolios for clients. That’s something the wealth management industry has always offered, of course—but usually only for the rich. An individual investor could open a brokerage account and assemble shares in maybe a few dozen companies, but achieving the diversification of an index by buying hundreds of stocks would have required a huge outlay with crushing commissions. Now a mix of dirt-cheap trading, powerful software, and the ability to buy fractions of shares is making the strategy available to a lot more investors.

There are two big selling points to customization: An investor can ditch companies they don’t like (or add ones they do), and they can sell individual losing stocks to help lower their tax bills. Those things aren’t possible in index ETFs, which have been winning the savings of Americans for more than a decade. So if a client works in tech and wants to trim her stock exposure to the sector so that both her career and portfolio aren’t subject to the same risks, she can do that. If she dislikes fossil-fuel companies, she could have a broad exposure to the S&P 500 but nix Exxon Mobil Corp. That’s a powerful lure when more investors are looking to consider environmental and social issues.

Selling losing stocks to offset a capital-gains tax bill can be an even bigger draw. A 2020 paper estimated that a strategy of well-timed tax-loss harvesting can help a U.S. investor’s portfolio beat a benchmark by about one percentage point—a significant boost when compounded over time.

Direct Indexing Didn’t Appear Overnight

Running a personalized portfolio used to be an expensive, time-consuming process, so the barrier to entry was high. Getting a separately managed account—which are used to house such strategies—at Dimensional Fund Advisors, for instance, typically required at least $20 million. That’s changing fast. In another nod to growing efficiencies, demand, and competition, Dimensional slashed the minimum to $500,000 in September. If that still sounds like the preserve of the rich, the likes of automated online wealth manager Wealthfront Corp. provide direct indexing for investors with as little as $100,000.

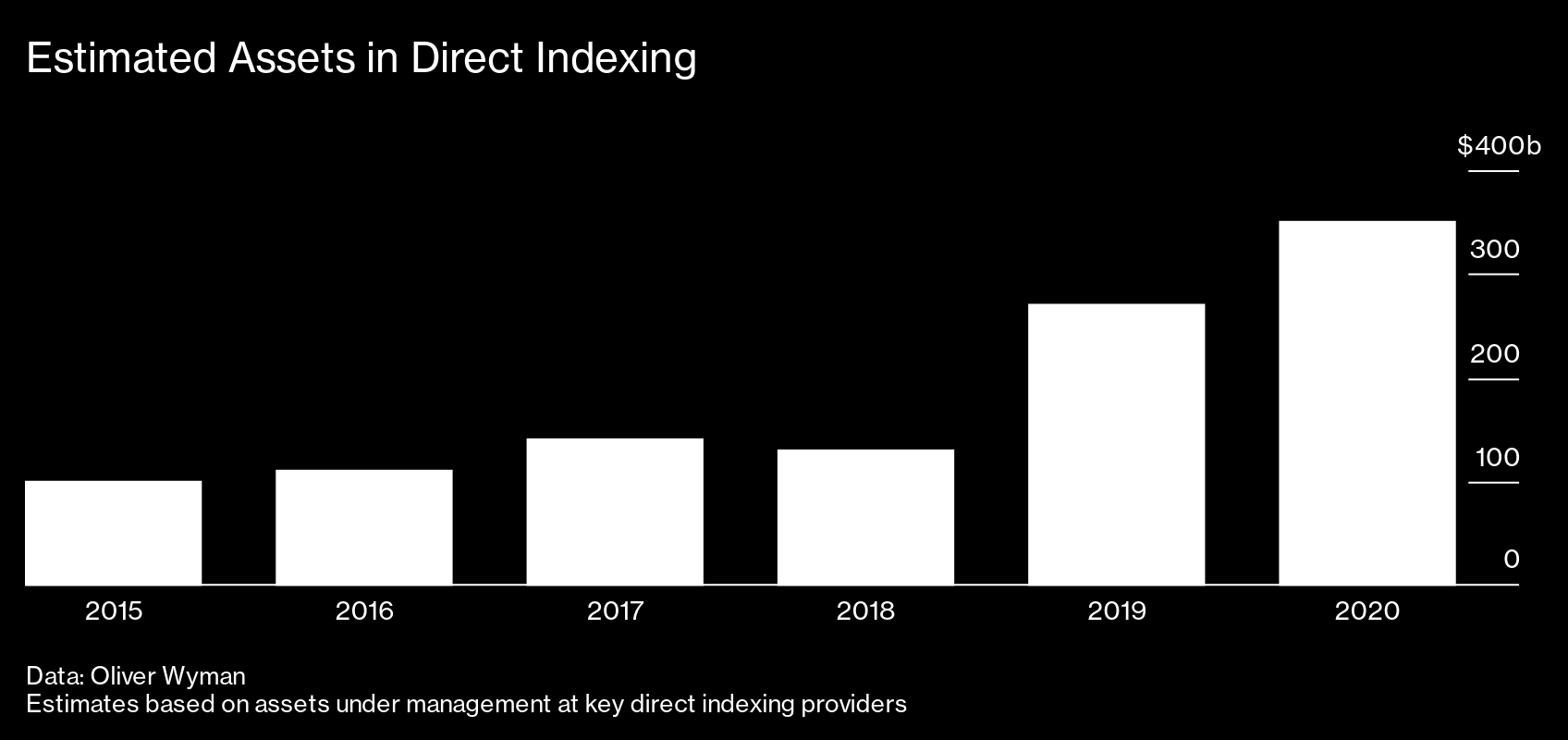

Direct indexing and custom indexing aren’t exactly the same things. With direct indexing, investors often start with an established benchmark, such as the S&P 500. But instead of buying shares of a fund that holds all the stocks in the index, they buy its individual members directly. Then they can tweak it to create their own versions of the benchmark. Morgan Stanley and Oliver Wyman estimated in a report this year that direct-indexing assets could reach $1.5 trillion in 2025 by seizing market share from mutual funds and ETFs, compared with $350 billion last year and $100 billion in 2015.

Estimated Assets in Direct Indexing

Data: Oliver Wyman

Estimates based on assets under management at key direct indexing providers

That’s why in May 2020 Charles Schwab Corp. acquired the technology of a firm called Motif that offered direct indexing. Then Morgan Stanley spent $7 billion on Eaton Vance Corp., which owned Parametric Portfolio Associates—one of the heavyweights in the investing style. Shortly after that deal, BlackRock Inc. announced it was buying Aperio, a creator of tailored index strategies, for $1 billion. Vanguard Group Inc. added direct indexer Just Invest in July—the first acquisition in its 46-year history. (Bloomberg LP, which publishes Bloomberg Businessweek, sells market indexes and portfolio analysis technology for the investment industry.)

At OSAM, Canvas is called custom indexing, rather than direct indexing. While clients can build portfolios based on an existing index, Canvas’s pitch is that they don’t necessarily have to. “The name was all about the idea it’s a blank canvas, and the adviser and the client get to paint their own picture exactly as they want, not something that’s off the shelf,” O’Shaughnessy says.

Stockpicking Doesn’t Have the Best Track Record

It’s easy to see why Wall Street loves tailored offerings of all stripes. For brokers and market makers, it fuels more trading flows. For asset managers, it’s a case to charge an average 0.3% of assets per year compared with 0.1% for ETFs, Bloomberg Intelligence estimates. For financial advisers, offering access to these programs is the latest way to preserve their 1% fee.

Skeptics warn the whole thing is a costly throwback for investors. After all, the evidence that active stockpicking can’t consistently beat the market is overwhelming. If even the pros can’t beat a benchmark, why would an individual do any better? “Every paper, every study in the world suggests people should not be involved in investing,” says Wes Gray at Alpha Architect, which offers ETFs as well as a direct-indexing service. He says the idea makes sense for a niche group of investors with specific needs, but doubts it will be helpful for most. “All these tools are going to empower the worst behavioral decisions,” he says.

And even that tax-loss harvesting strategy isn’t always great. It’s not necessary in tax-advantaged retirement accounts, where individual investors hold much of their wealth. And selling to offset tax incurs higher trading costs and causes deviations from the benchmark that will persist for at least a month, since U.S. wash-sale rules ban investors from buying back a security within 30 days. Meanwhile, for the tactic to be worth it, there must be a capital gain that needs offsetting. “There’s a pretty good argument that the costs and frictions are way higher than people think,” says Gray. “In 99% of the cases I cannot justify doing it.”

Custom Portfolios Pave the Way for Investing With ‘Personal Flair’

The string of mergers and acquisitions is a measure of just how fast custom indexing could grow, according to Michael Kitces, head of planning strategy at Buckingham Wealth Partners, which works with financial advisers. He says it could rapidly become a threat to ETFs and mutual funds, and he likens the change to last major industry shift. “That was the same story advisers had 15 years ago when the early players were recommending ETFs when everyone was still using mutual funds,” Kitces says. “When the industry decides to eat itself, change happens a whole lot faster.”

Change certainly came fast for OSAM, whose Canvas assets have doubled this year, to $2 billion. The firm has $5 billion under management in other products, but when Franklin Templeton announced the acquisition, it noted that the deal expanded its ability to offer custom portfolios. A longtime quantitative investor, O’Shaughnessy knows the research that drove trillions of dollars into index trackers. But in his telling, that revolution was never about being passive or simple; rather, it was about keeping costs down. Now tech has made it much cheaper for investors to treat their portfolios like fashion, mixing and matching with personal flair. “You can have low cost, you can have broad market exposure, you can have things like tax management,” he says. “You can have your cake and eat it too because of technology today.”

Read next:

The People and Ideas That Defined Global Business in 2021

"direct" - Google News

December 06, 2021 at 12:01PM

https://ift.tt/3xWPkb3

Wall Street Giants Bet on Direct Indexing to Take On ETFs and Mutual Funds - Bloomberg

"direct" - Google News

https://ift.tt/2zVRL3T

https://ift.tt/2VUOqKG

Direct

Bagikan Berita Ini

0 Response to "Wall Street Giants Bet on Direct Indexing to Take On ETFs and Mutual Funds - Bloomberg"

Post a Comment